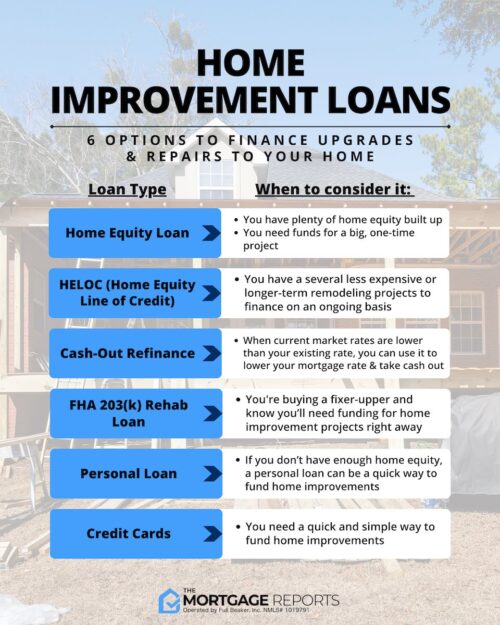

Stop treating your home equity like a magic piggy bank. A lot of people think the only way to fund a kitchen remodel or a new roof is to tap into a HELOC or a second mortgage, but that’s a massive mistake if you actually want to sleep at night. Tapping into your equity ties your debt directly to the roof over your head. If things go sideways, you aren’t just losing money; you’re risking your actual shelter.

There’s a cleaner way to handle upgrades without messing with your deed. We’ve spent plenty of time looking at how people actually fund these projects, and the math usually points toward unsecured personal loans. They’re faster, they don’t require a new appraisal, and they keep your home’s title clean. It’s a different way to think about debt, but it’s often the smarter move.

When you use a personal loan for a remodel, you aren’t borrowing against the house. You’re borrowing against your creditworthiness. That distinction matters. If you hit a rough patch, a personal loan sits in your debt column just like a credit card or an auto loan. It doesn’t trigger a foreclosure process the way a mortgage-backed product does. It’s a cleaner separation of risk.

Most people get caught up in the “how much can I borrow” phase before they even ask “how much do I actually need.” They see a huge lump sum and think they can do the kitchen, the bathroom, and the deck all at once. That’s a recipe for a high-interest disaster. You need to know exactly what the project costs before you ever walk into a bank.

Why Unsecured Loans Beat Equity-Based Debt

The biggest argument for an unsecured personal loan is speed. If your roof is leaking, you don’t have three weeks to wait for an appraiser to show up, value your property, and wait for a title company to run checks. You need a solution now. Personal loans can often be funded in a few days, sometimes even hours if your paperwork is ready.

We see homeowners get stuck in the “appraisal trap” all the time. To get a Home Equity Line of Credit (HELOC), you have to prove your home is worth significantly more than your current mortgage. If the market dips or your home value hasn’t spiked as much as you hoped, you’re stuck. A personal loan doesn’t care what your house is worth; it only cares about your income and your credit score. That makes the approval process much more predictable.

Then there’s the repayment structure. When you take out a home improvement loan, you get a fixed monthly payment. You know exactly when the debt will be dead. Many equity-based products have variable interest rates that can jump unexpectedly, turning a manageable monthly payment into a financial nightmare overnight.

Is the higher interest rate worth it for the peace of mind? For many, the answer is yes. You’re trading a slightly higher rate for the security of knowing your home’s title is safe. It’s a calculated trade-off. You’re essentially paying a small premium for flexibility and speed, which is smart when you’re dealing with urgent repairs.

Look at the numbers. While rates vary based on your credit, the amount you can access is significant. According to Bankrate, loan amounts for personal loans used for home improvement can range from $1,000 to $100,000. That’s wide enough to cover anything from a leaky faucet to a full basement conversion.

| Feature | Personal Loan | HELOC |

| Collateral | None (Unsecured) | Your Home (Secured) |

| Approval Speed | Fast (Days) | Slow (Weeks/Months) |

| Interest Rate | Fixed (Usually) | Variable (Usually) |

| Risk Level | Lower (Personal Asset) | Higher (Home Asset) |

Matching the Loan to the Specific Project

Not all renovations are created equal. You shouldn’t use the same financing strategy for a new roof that you use for granite countertops. This is where people trip up. Some projects are “defensive” repairs, things that protect the house. Others are “offensive” upgrades, things that make the house more enjoyable or increase its value.

If you’re dealing with an emergency like a broken furnace or a plumbing disaster, you need liquidity. A quick personal loan is perfect here. You don’t want to be negotiating terms with a bank while your basement is flooding. In these cases, speed is the only metric that matters. You need the cash in your account before the contractor’s invoice arrives.

For larger, long-term projects, you might want to look at how much you can borrow in a single lump sum. As noted by M&S Bank, choosing a personal loan lets you borrow the amount you need all in one go. This is helpful for big renovations like adding a sunroom, where the contractor expects a large upfront deposit and several progress payments.

There’s also a “green” angle. If you’re upgrading insulation, installing solar panels, or switching to a high-efficiency HVAC system, some lenders are more willing to work with you. Many people want to make their homes more sustainable without the financial stress. Using a loan specifically for energy efficiency can sometimes provide a better return on investment because those upgrades lower your monthly utility bills.

Consider these project types and the best way to fund them:

- Emergency Repairs: New roof, plumbing, electrical work. Use small, quick personal loans.

- Major Additions: Adding a bedroom or a new deck. Use large-scale personal loans or structured financing.

- Cosmetic Upgrades: New flooring, painting, or kitchen appliances. Use smaller, low-interest personal loans.

- Efficiency Upgrades: Solar panels or HVAC. Look for loans that allow for long-term repayment to offset energy savings.

If you want specialized advice on managing your debt during these transitions, check out texasloanstoday.com to see how different loan structures compare in different markets.

Avoiding the Debt Trap of “Scope Creep”

The most dangerous part of home improvement isn’t the interest rate; it’s the “while we’re at it” factor. You start out intending to replace the laminate countertops. Then you realize the cabinets are old. Then the backsplash needs to change. Then the lighting isn’t quite right. Suddenly, a $5,000 project is a $15,000 project.

This is how people end up maxing out their personal loans and still having an unfinished kitchen. It’s a psychological trap. When you have access to a large lump sum from a personal loan, it feels like “free” money until the invoices start hitting your inbox. You must set a hard ceiling before you even sign the loan agreement.

I recommend getting a “worst-case scenario” quote from your contractor before you apply for financing. Don’t get the quote for the perfect version of the room. Get the quote for the version where the subflooring is rotten and the electrical is outdated. That’s your real number. If you borrow more than that, you’re just paying for the privilege of stress.

One way to manage this is a “staged” approach. Instead of one massive loan, you might take a smaller personal loan for the immediate repairs, then take another one later for the cosmetic upgrades once you’ve seen how your budget handles the first payment. It keeps your monthly overhead lower and gives you more control.

It’s hard to be disciplined. It’s easier to be reckless. Most people fall into the second category because the temptation of a beautiful, finished home is very strong. But a beautiful home that comes with a crushing debt load is just a very expensive museum. You have to be the adult in the room when negotiating with your own desires.

The Hidden Costs of “Cheap” Money

When you’re comparing different loan offers, don’t just look at the APR. That’s a rookie mistake. The APR is important, but it doesn’t tell the whole story if there are massive upfront fees or prepayment penalties. Some lenders offer a low interest rate but charge a heavy origination fee that eats up the first three months of your payments.

Always ask about the “total cost of credit.” This is the actual amount of money you will have paid back by the time the loan is finished, including all interest and fees. Sometimes, a loan with a slightly higher interest rate but no origination fee is actually cheaper in the long run. Run these numbers on a spreadsheet, not just in your head.

Prepayment penalties are another silent killer. You want the freedom to pay off your loan early if you get a bonus or a tax refund. If your lender penalizes you for being responsible and paying the debt back ahead of schedule, they are essentially punishing your financial health. Avoid those lenders. You want a loan that works for you, not one that traps you into a specific timeline.

Finally, consider your credit score. Taking out a large personal loan will cause a temporary dip in your score because of the new inquiry and the shift in your debt-to-income ratio. If you’re planning to buy a new car or another home in the next six months, wait. If you’re settled in for the next few years, the dip is a minor blip on an otherwise long horizon.

The goal is to improve your life, not just your floor plan.

A few things readers ask

What is the difference between a personal loan and home improvement financing?

Personal loans are unsecured loans with fixed terms, while home improvement financing may involve a home equity loan or HELOC that uses your property as collateral.

Can I use a personal loan for home renovations?

Yes, personal loans are unsecured and can typically be used for any legal purpose, including kitchen remodels, roofing, or landscaping.

Is it better to use a personal loan or a home equity loan for home improvements?

Personal loans offer faster funding and easier approval, whereas home equity loans often provide lower interest rates and higher borrowing limits for large projects.

How does my credit score affect my personal loan for home repairs?

A higher credit score typically secures lower interest rates and better terms, reducing the total cost of your home improvement project.

Are there tax benefits to financing home improvements?

If the loan is used for capital improvements that add value to your home, the interest may be tax-deductible, but you should consult a tax professional for specifics.